|

Newsletter

Seminar Material

Biz:

China

Hong

Kong Hawaii

What people

said about us

China

Earthquake Relief

Tax &

Government

Hawaii Voter Registration

Biz-Video

Biz-Video

Hawaii's

China Connection

CDP#1780962

CDP#1780962

Doing Business in

Hong Kong & China

| |

Tax & Government Issue

-

Information from reliable sources

deemed reliable but "not" guaranteed

November 13 2008

Employers Beware: Under New Law, U.S.

Employees of Many Partnerships and Foreign Corporations May No Longer Be Able to

Defer Compensation

Beginning on January 1, 2009, commonly used nonqualified deferred compensation

arrangements may no longer be available to U.S. employees of certain

partnerships and foreign corporations (referred to herein as “Covered

Employers”). Legislation enacted on October 3, 2008 has added Section 457A to

the Internal Revenue Code (the “Code”). Section 409A of the Code (“Section

409A”) (enacted in 2004) already imposes many requirements and limitations on

nonqualified deferred compensation arrangements. However, new Section 457A of

the Code (“Section 457A”) may spell the end of U.S. federal income tax deferral

for compensation paid to U.S. employees by Covered Employers.

Hedge funds, whose U.S. managers are the primary target of Section 457A, will

naturally want to review the effect of the new rules on their deferred fee

arrangements and to monitor for upcoming regulations or other guidance that will

presumably address some of the uncertainties created by the new statute

(including, in particular, the uncertainties illustrated by the examples below).

However, all Covered Employers who may pay deferred compensation should also

carefully examine the potential application of the new statutory rules to their

employees subject to U.S. taxes, including U.S. citizens and U.S. residents, and

monitor for any new guidance with respect to these rules.

The New Law Ends Deferral or Imposes a Punitive Tax on Deferred Compensation

The new law introduces two basic rules for “deferred compensation” (i.e.,

compensation deferred for a period of more than 12 months following the year in

which it is earned) received from a Covered Employer. First, deferred

compensation is taxable once it is “vested.” Deferred compensation is vested

when it is no longer subject to a substantial risk of forfeiture (generally,

once the right to compensation is no longer contingent upon the performance of

“substantial” future services). Second, if at the time of vesting the amount of

deferred compensation is not determinable, it is included in income when it

becomes determinable. However, at the time the amount becomes determinable, it

is also subject to an additional 20% tax plus interest.

The New Law Targets Hedge Fund Managers, But…

Section 457A targets a structure commonly used to defer fee income received by

managers of offshore hedge funds. In a typical offshore hedge fund structure, a

fund manager (generally organized as either a foreign corporation or

partnership) earns fee income from the funds it manages and, in turn, pays

compensation to the individuals who provide the management services on its

behalf. The compensation arrangements also frequently include non-qualified

deferred compensation plans that allow the individuals to defer all or a portion

of their compensation, subject to the limitations of Section 409A. Under Section

457A, this deferral opportunity will be substantially eliminated.

The Broad Reach of the New Law Extends to Many Other Types of Employers

The scope of Section 457A is much broader than just hedge fund managers, in

large part as a result of the statutory definition of “Covered Employers” whose

compensation arrangements are subject to the new rules. Under Section 457A,

Covered Employers include, with limited exceptions, all non-U.S. corporations

unless substantially all of their income is subject to a “comprehensive foreign

income tax.” It therefore generally includes, among others, all corporations

organized in offshore jurisdictions like the Cayman Islands, Bermuda or the

British Virgin Islands. It also includes any partnership, whether domestic or

foreign, any meaningful amount of whose income is allocated to partners who are

either U.S. tax-exempt organizations or non-U.S. persons not subject to a

“comprehensive foreign income tax” with respect to such income.

“Side Pocket” Arrangements

Section 457A authorizes regulations that would treat deferred fees with respect

to certain single-investment “side pocket” arrangements as being unvested until

the side pocket’s sole investment is sold (which would prevent the application

of the additional 20% tax and interest charge). However, no such regulations

have been issued so far. Furthermore, it remains unclear how this special rule

will interact with the rules of Section 409A. Treatment of side pocket

arrangements will remain uncertain until the Treasury Department issues guidance

that activates the special rule and addresses the interrelation between Sections

409A and 457A with respect to single-investment side pocket compensatory

arrangements.

Examples

To better understand what the new rules mean as a practical matter, consider the

following common scenarios:

1. Deferred Hedge Fund Fees:

Andrew is a U.S. citizen employed by Investco. Investco is a foreign hedge fund

manager and is a Covered Employer. Investco agrees to pay Andrew annual

compensation in an amount equal to a specified percentage of the fund’s net

income (his “Fees”). Andrew is entitled to (and does) defer this compensation

under an arrangement that complies with Section 409A. Deferred Fees accrue

earnings at a rate that reflects the rate of appreciation of the fund’s assets.

The deferred Fees, together with earnings thereon, are payable at the earlier of

the time that Andrew terminates his employment with Investco or the time that

the fund is liquidated.

In this example, Andrew’s right to his deferred Fees and any earnings that may

be credited to those deferred Fees is “vested” (that is, not subject to a

substantial risk of forfeiture) at the time he performs the services.

Accordingly, under the first rule of Section 457A, Andrew should be subject to

tax on the amount of his deferred Fees in the year that he performs the services

to which those deferred Fees are attributable. However, the total amount of the

earnings that he will receive is not determinable because they depend on the

performance of the fund. As a result, it is not clear how the Internal Revenue

Service (the “IRS”) will apply the second rule of Section 457A. The IRS most

likely will determine that the amount of the deferred Fees is determinable and

included in Andrew’s income at the time it is earned and credited to his account

each year and that any earnings on the deferred Fees are determinable and

included in his income as they are earned and credited to his account each year.

(Under this scenario, it is not clear how the losses would be treated -- perhaps

Andrew would not be allowed any deduction for losses but would not include

additional earnings in income until after he recoups prior losses through

additional earnings.) Alternatively, the IRS may determine that the amount of

the deferred Fees is determinable and included in his income each year, but the

amount of earnings to be paid to him in the future is not determinable until the

final payment date (because of potential losses and unknown future earnings). In

that case, the amount of earnings would not be taxable until paid to him in the

future. (This treatment would be analogous to the treatment of earnings after

vesting under deferred compensation plans of governmental entities and tax

exempt organizations under Section 457(f) of the Code.) Under this analysis, the

earnings would be subject to the additional tax of 20% plus interest in at the

time of payment. Finally, though not very likely, the IRS may determine that the

total amount of the deferred Fees and earnings thereon is not determinable until

paid. Under that analysis, Andrew would not pay any tax on either the deferred

Fees or the earnings on the deferred Fees until all of the deferred compensation

is paid, but it would all be subject to the additional tax of 20% plus interest

when paid.

2. Defined Benefit Deferred Compensation:

Employee Betty is a U.S. taxpayer who works for foreign corporation, Caymanco.

Caymanco is organized in the Cayman Islands (one of a number of jurisdictions

that do not have a comprehensive income tax system) and is thus a Covered

Employer. Caymanco provides Betty with a nonqualified supplemental executive

retirement plan (“SERP”). The SERP benefit is based on a percentage of Betty’s

final average pay and years of service. The benefit vests after 5 years of

service. Upon vesting, Betty will not know the amount of her SERP benefit

because she may have future earnings and years of service that will affect the

amount of the benefit.

Because the benefit is not determinable upon vesting, under Section 457A, Betty

does not have taxable income at vesting, but will be taxed at ordinary income

tax rates, incur an additional 20% tax and bear an interest charge when the

amount of her benefit can be determined (i.e., upon her retirement).

3. Elective Deferrals:

Assume the same facts as in Example 2, except Caymanco provides Betty with a

nonqualified deferred compensation plan under which Betty may elect to defer up

to 30% of her salary, payable upon termination of employment. Caymanco will

match her deferrals up to 5% of her salary, subject to a 3-year vesting

requirement. Under this arrangement, Betty’s account balance payable upon

termination will include the aggregate of her deferrals and matching

contributions, adjusted for earnings or losses thereon based on various

investment options chosen by Betty.

Prior to the enactment of Section 457A, Betty generally would have been able to

defer tax on her deferred compensation until termination of her employment.

However, Section 457A significantly alters this result. Since Betty is always

vested in her elective deferrals, such amounts should be taxable immediately

under Section 457A in the year that she earns the salary (thus defeating the

purpose of the deferral arrangement). With respect to the matching

contributions, Betty should first become taxable on the accumulated matching

contributions when she becomes vested in year 3 under the first rule of Section

457A, and each matching contribution after vesting should be taxable at the time

it is credited to her account. However, the precise amount of all or a portion

of Betty’s ultimate deferred compensation benefit may be viewed as not

determinable until paid due to the continuing adjustment for earnings and losses

as discussed with respect to Andrew’s deferred Fees in Example 1. Forthcoming

regulations will likely explain which of the three alternatives described in

Example 1 will apply for determining the timing of the taxation of Betty’s

deferred compensation. However, we expect the most likely result is that (1) her

own deferrals will be taxed as they are earned and credited to her account each

year, (2) the amount of accumulated matching contributions through the vesting

date, together with earnings thereon, will be taxed at the vesting date and

subsequent matching contributions will be taxed as they are credited to her

account, (3) earnings on her own deferrals will be taxed as they are credited to

her account, (4) earnings on the matching contributions after the vesting date

will be taxed as they are credited to her account and (5) special rules will

address how to deal with losses.

Effective Dates

The rules of Section 457A generally apply only to compensation for services

performed on or after January 1, 2009. However, deferred compensation amounts

relating to services performed prior to that date do not escape Section 457A.

Rather, such amounts will be includible in income no later than 2017 (or, if not

yet vested by that point, upon vesting).

This memorandum is a summary for general information and discussion only and may

be considered an advertisement for certain purposes. It is not a full analysis

of the matters presented, may not be relied upon as legal advice, and does not

purport to represent the views of our clients or the Firm. Linda Griffey, Luc

Moritz, Summer Conley, and Bryan Kelly contributed to the content of this

newsletter. The views expressed in this newsletter are the views of the authors

except as otherwise noted.

Portions of this communication may contain attorney advertising. Prior results

do not guarantee a similar outcome. Please direct all inquiries regarding our

conduct under New York's Code of Professional Responsibility to O’Melveny &

Myers LLP, Times Square Tower, 7 Times Square, New York, NY, 10036,

Phone:+1-212-326-2000. © 2008 O'Melveny & Myers LLP. All Rights Reserved.

IRS Circular 230 Disclosure

To ensure compliance with requirements imposed by the IRS, we inform you that

any U.S. tax advice contained in this communication (including any attachments)

is not intended or written to be used, and cannot be used, for the purpose of (i)

avoiding penalties under the Internal Revenue Code, or (ii) promoting, marketing

or recommending to another party any matters addressed herein.

June 11 2008

Social Security is pleased to announce

that the enrollment period for the Consent Based Social Security Number (SSN)

Verification (CBSV) service has been extended through June 30, 2008.

Social Security is pleased to announce

that the enrollment period for the Consent Based Social Security Number (SSN)

Verification (CBSV) service has been extended through June 30, 2008.

As you know, CBSV is a fee-based SSN verification service that will permit

private businesses, Federal, State, and local governments to verify an

individual’s SSN once a valid and signed consent form is obtained from the SSN

holder. This letter is being sent to you because you and/or your affiliates may

have an interest in enrolling in this service. Service will begin October 2008.

If you are interested in more information about CBSV, click on, http://www.socialsecurity.gov/bso/cbsvMarketing.html

If you have any questions you may write to SSA.CBSV@ssa.gov.

We hope you will find this service useful and look forward to the opportunity to

discuss this exciting new project with you.

Sincerely,

Cheri Arnott

Associate Commissioner for External Affairs

June 11 2008 June 11 2008

ATTENTION ALL Hawaii QHTB'S - Tax

Filing Deadline for N-317 June 30th

The deadline for filing the new on-line N-317 is June 30th. Two critical reasons

for filing on time:

1. The penalty for not filing is $1,000 per month up to $6,000.

2. The data DoTax receives from industry will be critical in the discussion on

the renewal of Act 221/215.

Visit the DoTax site home page http://hawaii.gov/tax/ and look for "E-File

Login" for instructions.

|

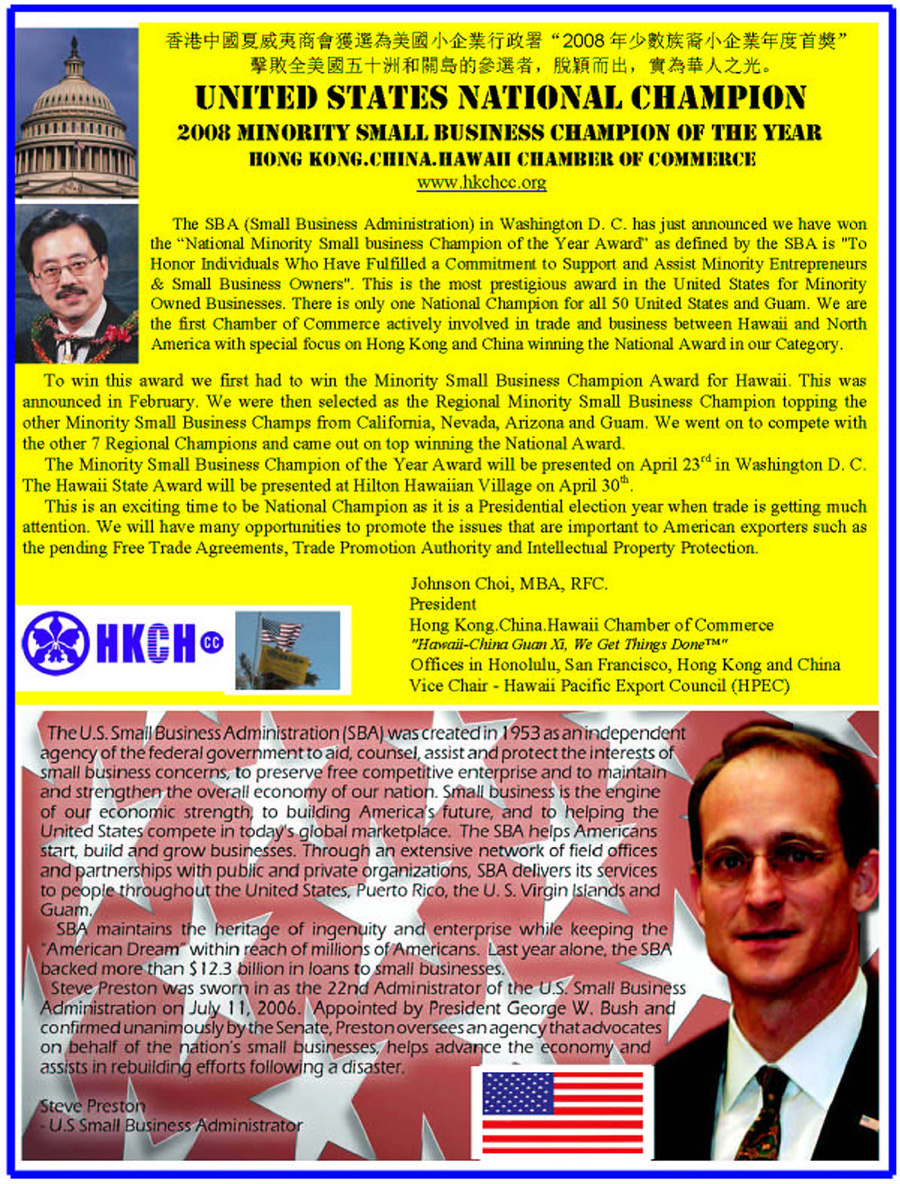

USA Small Business Administration (SBA)

Selected Johnson Choi/HKCHcc

2008 United States

National Champion

USA Small Business Administration (SBA)

Selected Johnson Choi/HKCHcc

2008 United States

National Champion